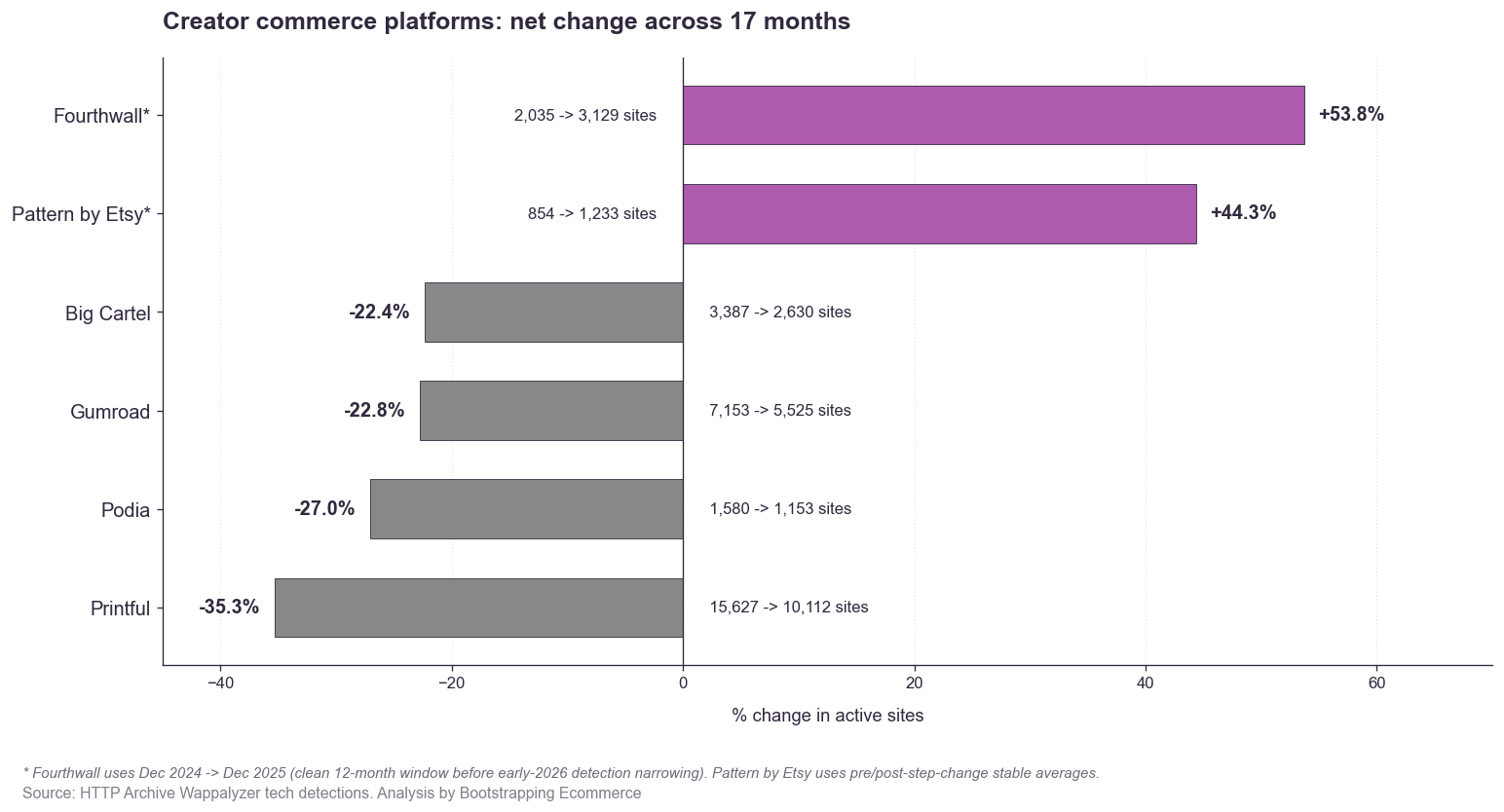

Two of the six creator commerce platforms we tracked grew strongly over the past 17 months. The other four lost between 22% and 35% of their active sites.

- Fourthwall climbed steadily through 2025 to +54% by December of that year, the largest real growth in our dataset.

- Pattern by Etsy grew approximately +44% on a conservative read of its data, riding Etsy’s marketplace traffic.

- Big Cartel, Gumroad, Podia, and Printful each lost a fifth or more of their deployed sites.

The pattern under the ranking is straightforward: platforms with built-in audience flows held their ground. The pure standalones didn’t.

Here is the ranking:

- Fourthwall: +54% over a clean 12-month window (Dec 2024 to Dec 2025), supported by strong creator-economy positioning with YouTube, Twitch, and podcast audiences

- Pattern by Etsy: +44% on a conservative pre/post-step-change baseline, riding Etsy’s marketplace traffic

- Big Cartel: -22.4%

- Gumroad: -22.8%

- Podia: -27.0%

- Printful: -35.3%

The numbers come from HTTP Archive’s Wappalyzer tech-detections table on Google BigQuery, the same public dataset the Web Almanac is built on. Seventeen monthly snapshots, mobile crawl, roughly 28 million pages per month.

The rest of this piece walks through the leaderboard, the trajectories, the funnel mechanics, a close-up on Printful, what Pattern by Etsy’s growth tells you about where sellers are going, and what any of this should change about your own platform decision.

Where the Numbers Come From

HTTP Archive crawls millions of pages every month and publishes the raw data to Google BigQuery. Wappalyzer fingerprints platforms by HTML signatures, response headers, JavaScript variables, and DOM patterns. The wappalyzer.tech_detections table rolls those detections up into monthly counts of active sites per technology, plus adoption and churn flows.

We pulled 17 monthly snapshots, December 2024 through May 2026, for six creator-commerce platforms. Documentation lives at the HTTP Archive Web Almanac and the Wappalyzer technology docs.

Two of the six platforms had Wappalyzer detection-rule changes inside the window, so we use each platform’s longest clean reading window rather than forcing a single arbitrary period on all six.

- Fourthwall. A fingerprint update between November and December 2024 dropped the count from 23,706 to 2,035 sites overnight. A second narrowing arrived in early 2026. We use the clean 12-month window Dec 2024 to Dec 2025 (2,035 to 3,129 sites, +54%) as Fourthwall’s reliable read, and we cross-validate it below.

- Pattern by Etsy. Three visible step-changes (Oct 2025, Dec 2025, Apr 2026). The conservative read uses pre-step-change vs post-step-change stable averages (854 -> 1,233 = +44%). The naive Dec ’24 to May ’26 endpoint gives +17.2%. Both land on growth.

Cross-validating Fourthwall against independent sources

Detection-rule changes are an inference unless something independent confirms or refutes them. For Fourthwall, two outside data points line up with the HTTP Archive clean-period growth and rule out a real decline:

- Storeleads, an independent retail tracker that detects live storefronts via DNS data (a different methodology than Wappalyzer’s HTML fingerprinting), reports Fourthwall stores growing from 11,767 in Q4 2024 to 19,212 in Q1 2026 (+63%) and continuing to 20,462 by June 2026, with +44% year-on-year growth into Q1 2026.

- Fourthwall’s own public communications, including a January 4 2026 blog post announcing 200,000 sellers on the platform and Phil DeFranco joining as Chief Creator Officer, do not fit a company that just lost a quarter of its merchants in the same month.

Both independent signals agree on continued growth into 2026 at roughly the same rate the HTTP Archive clean window shows. The Wappalyzer late-2026 cliff is the outlier with no corroborating signal anywhere else, which is why we treat it as a fingerprint narrowing rather than a real flow.

From here on, the numbers are the numbers and the story is the story.

The Six-Platform Leaderboard

Of the six platforms we tracked, two grew strongly, four lost a fifth or more of their deployed sites.

| Platform | Reading window | Start | End | Change |

|---|---|---|---|---|

| Fourthwall | Dec 2024 -> Dec 2025 (clean 12 mo) | 2,035 | 3,129 | +53.8% |

| Pattern by Etsy | Pre/post-step stable averages | 854 | 1,233 | +44.3% |

| Big Cartel | Dec 2024 -> May 2026 (17 mo) | 3,387 | 2,630 | -22.4% |

| Gumroad | Dec 2024 -> May 2026 (17 mo) | 7,153 | 5,525 | -22.8% |

| Podia | Dec 2024 -> May 2026 (17 mo) | 1,580 | 1,153 | -27.0% |

| Printful | Dec 2024 -> May 2026 (17 mo) | 15,627 | 10,112 | -35.3% |

Fourthwall is the largest real grower in the dataset. It added a net 1,094 sites over 12 months of clean, steady monthly growth, averaging +91 sites per month with no big spikes or dips. The Dec 2024 to Dec 2025 trajectory is the cleanest growth signal across all six platforms, and it sits on top of Fourthwall’s strong positioning with content creators (YouTube, Twitch, podcasting), whose audiences carry directly into the storefront.

Pattern by Etsy is the marketplace-backed grower. Pattern is the storefront product Etsy offers sellers who want their own URL alongside marketplace listings, so the Etsy traffic and trust ride along. The +44% conservative read holds even after stripping the noisy detection-change months.

Printful is the steepest decline by far. It lost 5,515 net active sites, more than the next three decliners combined (Gumroad 1,628, Big Cartel 757, Podia 427). The platform with the biggest brand awareness in print-on-demand is also the platform losing merchants fastest.

The four decliners cluster tightly inside a 13-point band. Big Cartel at -22.4%, Gumroad at -22.8%, Podia at -27.0%, Printful at -35.3%. Print-on-demand, digital downloads, indie merch, and online courses are all moving in the same direction at roughly the same speed. That uniformity is the strongest signal in the dataset: the pressure is on the standalone-creator-platform category, not on any individual product.

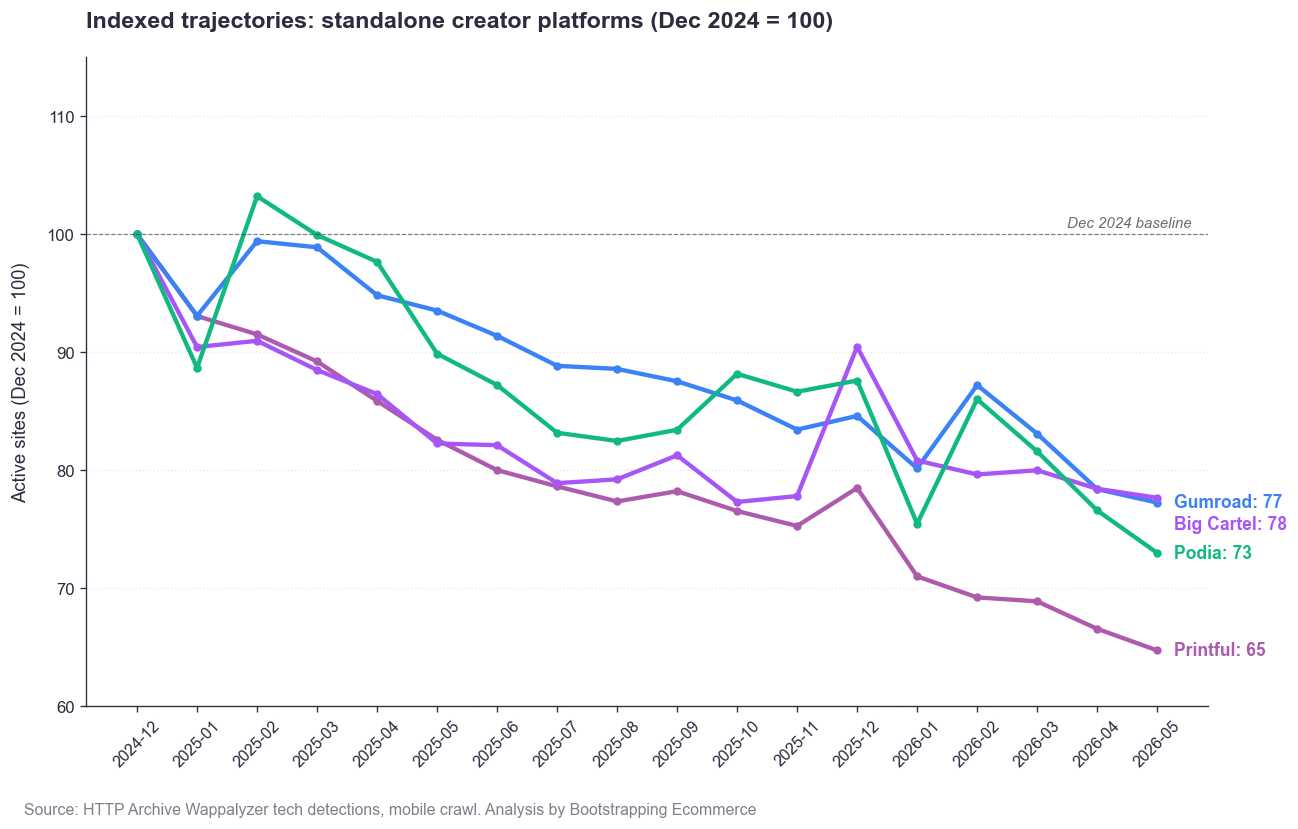

The Indexed Trajectories

Indexed to December 2024, here is how each of the four declining platforms trended through May 2026.

Indexed trajectories: standalone creator platforms (Dec 2024 = 100)

Printful

Closed at 65 against a December 2024 baseline of 100. The steepest curve in the chart. The big step-down between December 2025 and January 2026 lines up with seasonal churn after the holiday push, when seasonal storefronts stop trading.

Gumroad

Closed at 77. Less steep than Printful but flat-to-down throughout. The slope settles around mid-2025 and never lifts. No recovery signal.

Big Cartel

Closed at 78, almost identical to Gumroad. Two platforms selling to very different audiences (indie artists vs digital creators) ending the window within a single index point of each other tells you the pull is on the category, not the product.

Podia

Closed at 73. The smaller base means monthly crawl noise is louder, so the line wobbles. The trend is consistently down.

No recovery in any of the four. The decline is spread evenly across the 17 months on every platform, not concentrated in a single shock event. Whatever is pulling on the standalone category is doing it continuously.

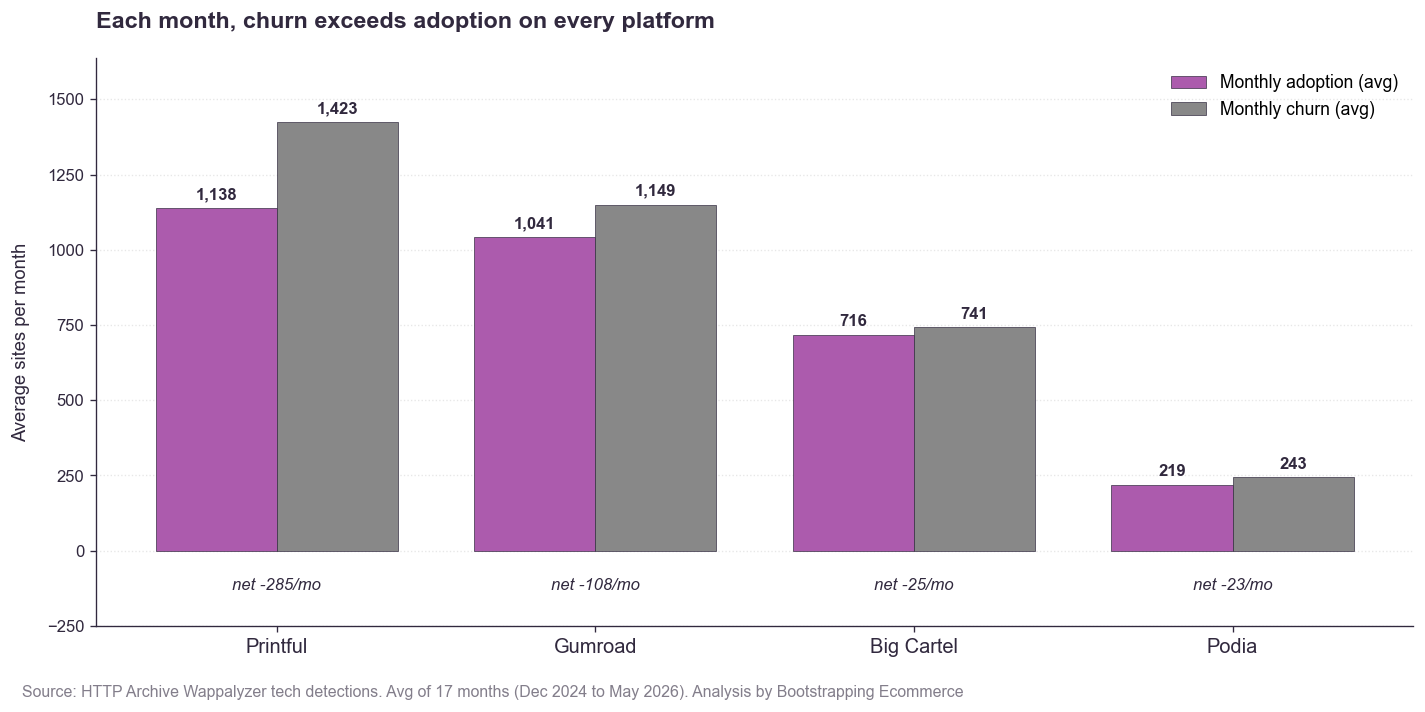

Why It’s Happening: Adoption Is Steady, Churn Just Beats It

These platforms are not in collapse. Each one still gains roughly the same number of new sites per month as it did at the start of the period. The decline is on the back end of the funnel, where existing storefronts go dark slightly faster than new ones come online.

Each month, churn exceeds adoption on every platform

| Platform | Avg adoption/mo | Avg churn/mo | Net/mo |

|---|---|---|---|

| Printful | 1,138 | 1,423 | -285 |

| Gumroad | 1,041 | 1,149 | -108 |

| Big Cartel | 716 | 741 | -25 |

| Podia | 219 | 243 | -23 |

Printful runs the widest funnel and the widest net deficit. Around 1,138 sites adopt Printful in an average month; around 1,423 churn off. That 285-site monthly gap multiplied by 17 months explains most of the 5,515-site decline.

Gumroad runs a tighter funnel. Net minus 108 a month. The leak is real but narrow enough that a single quarter of stronger adoption could flip the line.

Big Cartel and Podia are nearly stable. Net minus 25 and minus 23 a month against bases of a few thousand sites is barely a leak. If churn dropped by 30 sites a month on either platform, the line would flatten.

The takeaway: no platform is seeing churn collapse, and no platform is seeing adoption acceleration. The category is contracting slowly and uniformly across very different products. That uniformity is what makes this a category story, not a product story.

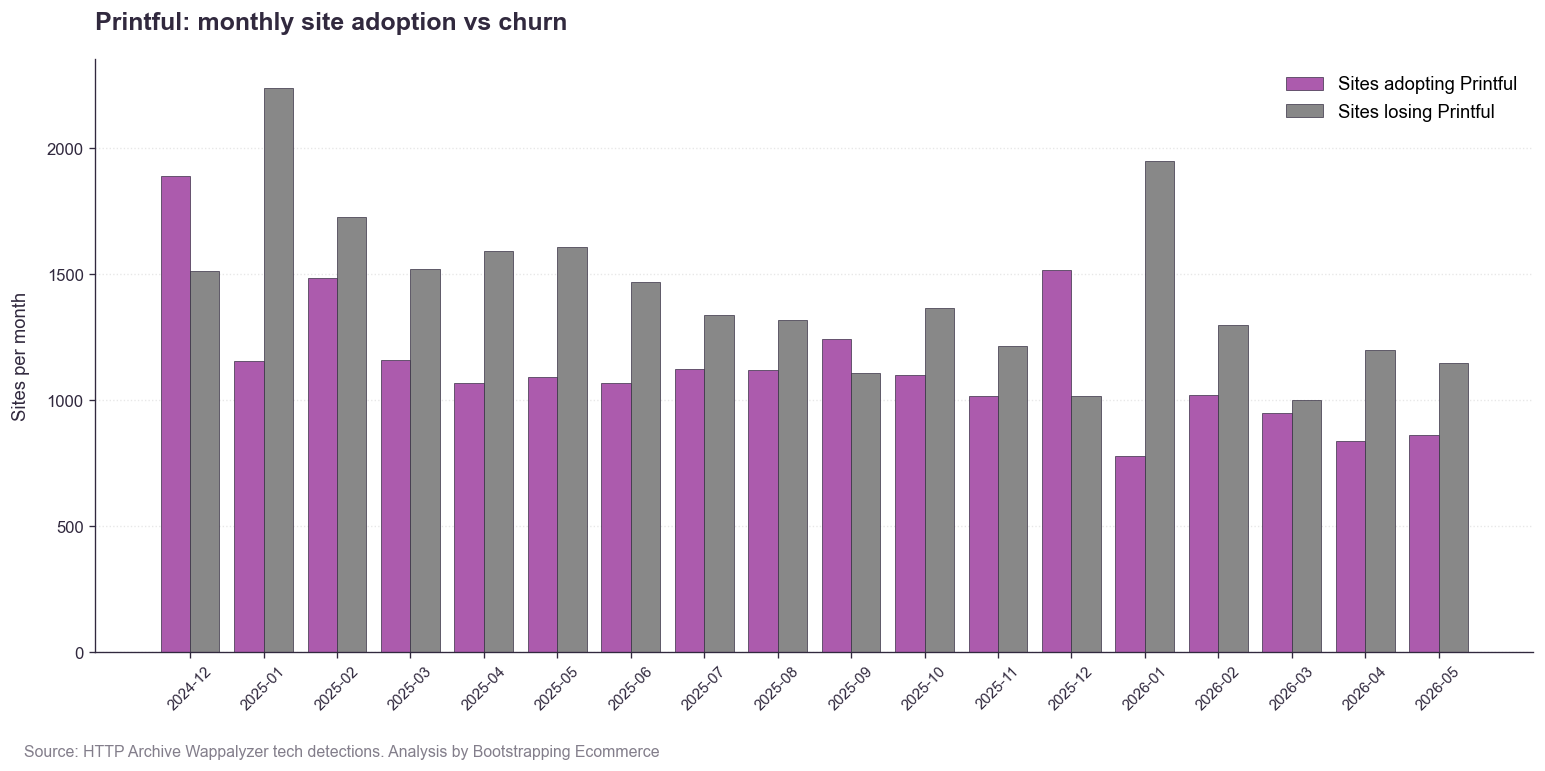

Printful in Detail

Printful is the platform BE readers ask about most. The detail chart shows why the decline is real without overstating it.

Printful monthly site adoption vs churn

- Adoption stayed near 1,100 sites per month with relatively little drift. New merchants are still choosing Printful regularly.

- Churn averaged 1,423 sites per month and ran above adoption in every month of the dataset. There is no recovery month.

- The biggest churn months cluster after the November holiday push, suggesting some Printful stores stop trading once their seasonal volume ends rather than migrating to a competitor.

The right interpretation is not “Printful is dying.” It is “Printful is the default workshop for a category of seasonal and casual storefronts that are now closing slightly faster than new ones open.”

For comparing POD backends specifically, our Printful vs Printify breakdown covers the side-by-side. For the broader Shopify-integrated POD stack, the roundup of the best Shopify print-on-demand companies walks through which providers are shipping reliably this year.

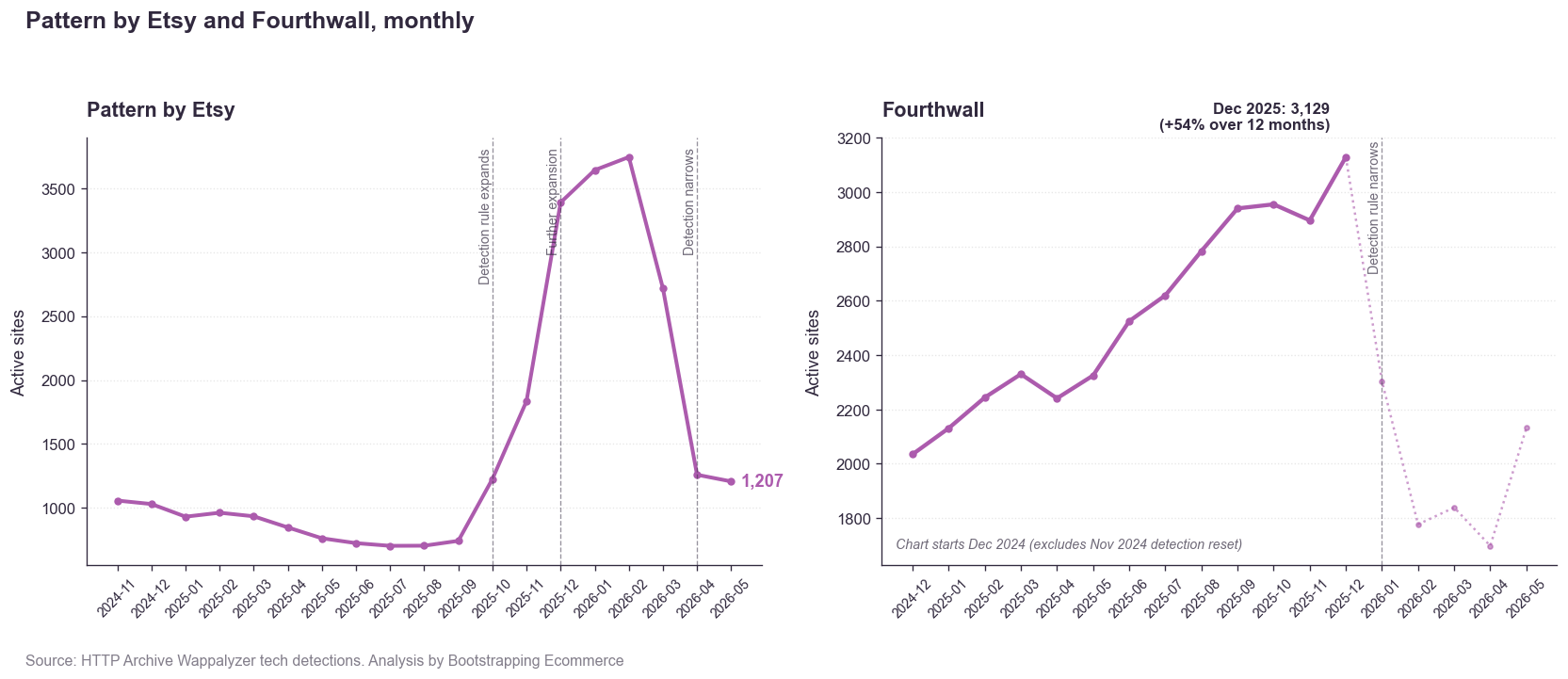

What Pattern by Etsy and Fourthwall Tell Us About Where Sellers Are Going

Both growers in the dataset share a common thread: built-in audience or creator-economy flows the pure standalones don’t have.

Pattern by Etsy and Fourthwall, monthly

Pattern by Etsy: marketplace gravity is real

Pattern is the storefront product Etsy offers sellers who want their own URL alongside marketplace listings. The growth signal here is attached to a marketplace, and that is the cleanest version of the broader thesis in this dataset.

Etsy itself reports approximately 9 million active sellers globally in its investor disclosures, and Etsy.com receives hundreds of millions of monthly visits. A Pattern storefront inherits all of that distribution.

The trade-offs are real. Etsy charges listing fees, transaction fees, and payment processing on top of each other, and the marketplace owns the customer relationship rather than the seller. The fee math behind that is in our breakdown of how much commission Etsy takes.

Fourthwall: the cleanest growth signal in the dataset, confirmed by independent data

Fourthwall climbed steadily from 2,035 sites in December 2024 to 3,129 sites in December 2025, a +54% gain spread across 12 months of consistent monthly growth. The trajectory averaged +91 sites per month with no spikes and no dips.

This is the cleanest real-growth curve in our dataset, and it is confirmed by two independent sources that don’t depend on Wappalyzer at all:

- Storeleads, an independent retail tracker, reports Fourthwall stores at 11,767 in Q4 2024 growing to 19,212 in Q1 2026 (+63%), with +44% year-over-year growth continuing into Q1 2026.

- Fourthwall publicly announced 200,000 sellers on the platform in a January 2026 blog post that also confirmed Phil DeFranco joining as Chief Creator Officer.

The pull behind the growth is identifiable. Fourthwall has earned strong positioning with content creators on YouTube, Twitch, and podcasting, and its merch-and-membership stack pairs naturally with audiences those creators already own. A creator with an existing audience plus a Fourthwall storefront skips the hardest part of running a standalone shop, which is sourcing the first thousand visitors. That audience-side integration is what the data is rewarding.

What This Means for You

The data is clear on direction. The translation to your decision depends on where you are starting.

If you’re already on one of these platforms

The data does not say to migrate. Printful losing 35% of deployed sites still leaves a working business with thousands of new monthly adoptions. If your store works, the platform is not the problem.

If you are considering a move:

- Etsy works for POD if you accept the fees and the customer-ownership trade-off. Our guide to the best print-on-demand companies for Etsy covers the practical setup.

- Shopify works if you want a standalone storefront with positive momentum. Our companion analysis showed Shopify gaining 79,000 net live storefronts in the same window.

- Big Cartel and Podia owners with stable revenue can stay put. The absolute net loss is small enough that the category contraction has not really hit your store yet.

If you’re starting a new store in 2026

The data points away from the older standalone platforms. Two real options stand out:

- Etsy first, especially for POD or handmade. Lowest friction, marketplace traffic baked in. Pattern by Etsy gives you an owned URL if you want one without leaving the marketplace.

- Shopify if you want full ownership of your storefront and you can drive traffic. Our Shopify vs Squarespace vs Wix breakdown is the next step for that comparison.

For digital products specifically, the standalone-platform category is the weakest of the three options. Our Gumroad alternatives roundup covers the live options. If your product is wearable art or marketplace-style merch, the Redbubble alternatives guide sits alongside it.

If you’re a creator-economy investor or operator

The standalone-platform category is contracting at a steady, measurable rate. Adoption and churn are running close to one another, and churn wins every month on the four decliners.

Pattern by Etsy’s marketplace-backed growth and Fourthwall’s steady +54% climb both point at the same dynamic. Platforms with built-in audience flows are outperforming pure standalones. The category is not collapsing; it is consolidating around platforms that bring sellers something more than infrastructure.

Frequently Asked Questions

Is Printful dying in 2026?

No, but Printful’s deployed footprint shrank 35.3% between December 2024 and May 2026, from 15,627 sites to 10,112. About 1,138 sites adopt Printful in an average month; about 1,423 churn off. Slow contraction, not collapse.

Is Pattern by Etsy really growing?

Yes. The naive Dec ’24 to May ’26 comparison gives +17.2%, and the conservative pre/post-step-change baseline gives +44%. Either way, Pattern is the only platform in our sample whose detected site count ended higher than it started.

What happened to Fourthwall?

Fourthwall is the cleanest growth story in the dataset. HTTP Archive shows +54% Dec 2024 to Dec 2025. Independent retail tracker Storeleads reports the same business at +63% over a similar window (Q4 2024 to Q1 2026), with growth continuing into Q2 2026. Fourthwall itself announced 200,000 sellers on the platform in a January 2026 blog post. All three sources point at the same trajectory.

Is Gumroad still worth using in 2026?

It depends what you sell. Gumroad lost 22.8% of deployed sites in 17 months but is still adopted by roughly 1,041 new sites per month. For digital downloads with a creator-friendly checkout, it remains a real option.

Where do creators go when they leave Printful, Gumroad, Big Cartel, or Podia?

The HTTP Archive data does not directly track migrations, but two destinations stand out. Shopify gained 79,000 net live storefronts in the same window in our companion analysis. The Etsy marketplace reports approximately 9 million active sellers globally, with Pattern by Etsy giving sellers an owned URL alongside their listings. The fee math is in our Etsy commission breakdown.

What’s the source data?

HTTP Archive’s wappalyzer.tech_detections public BigQuery table, monthly snapshots December 2024 through May 2026. The dataset is free to query.